Published: June 9, 2026 · Last updated: June 9, 2026

America’s Biggest Banks Are Building Their Own Blockchain: What “Tokenized Deposits” Mean for Your Money

For years, the largest banks in America treated blockchain like a fad for crypto traders. This month they quietly admitted it is the future of money movement. JPMorgan, Bank of America, Citigroup, Wells Fargo and other major lenders are building a shared “tokenized deposit” network, and they are doing it for one blunt reason: to stop stablecoins from draining money out of your bank account.

This article is for informational purposes only and does not constitute financial advice. Always consult a qualified financial advisor before making decisions about your money.

What This Article Covers

- What the banks actually announced

- What a “tokenized deposit” even is

- Tokenized deposit vs. stablecoin

- Why they are building it right now

- What changes for you, and what doesn’t

- Three kinds of digital dollar, side by side

- Frequently asked questions

JPMorgan, Bank of America, Citigroup, Wells Fargo and other lenders are building a shared tokenized deposit network through The Clearing House, targeting the first half of 2027, to allow 24/7 blockchain settlement of deposits without the money leaving the regulated banking system. It is a defensive move against stablecoins, which Jefferies estimates could drain 3%–5% of core bank deposits over five years. A tokenized deposit is still a dollar in your FDIC-insured bank, just one that can move instantly, any hour, any day. It is a better checking account, not money you hold yourself.

Quick Takeaways

- Major U.S. banks are jointly building a tokenized deposit network via The Clearing House.

- Target launch is the first half of 2027, enabling 24/7 blockchain-based settlement.

- The money stays inside the regulated, FDIC-insured banking system.

- It is an explicitly defensive answer to stablecoins eating into bank deposits.

- For you it means faster, around-the-clock transfers, but it is still a claim on a bank.

- The fact that banks are racing to build this tells you which idea they actually fear.

What the Banks Actually Announced

JPMorgan Chase, Bank of America, Citigroup, Wells Fargo and other major lenders are building a shared tokenized deposit network through The Clearing House, the real-time payments company the big banks collectively own. The effort targets the first half of 2027 for 24/7, blockchain-based settlement of customer deposits while keeping the underlying funds within the regulated banking system, according to CoinDesk. The Wall Street Journal first reported the plan on June 5, with the shared, bank-owned structure confirmed shortly after (Blockhead).

The headline word is “shared.” These banks compete fiercely for your deposits, yet they are pooling effort on the plumbing, the same way they already co-own real-time payment rails. That cooperation is the tell: they see a common threat and are answering it together.

What a “Tokenized Deposit” Even Is

Strip away the jargon. A tokenized deposit is an ordinary bank deposit, a dollar sitting in your checking or savings account, recorded on a blockchain ledger instead of a traditional one. It stays inside the regulated system, carries your bank’s credit profile, passes the usual identity and anti-money-laundering checks, and remains FDIC-insured (Brookings).

What the “token” part buys you is movement. Because the dollar is now a programmable entry on a shared ledger, it can settle in seconds, at 3 a.m., on a Sunday, on a holiday, none of which the current system does well. The dollar does not change. The rails it rides on do.

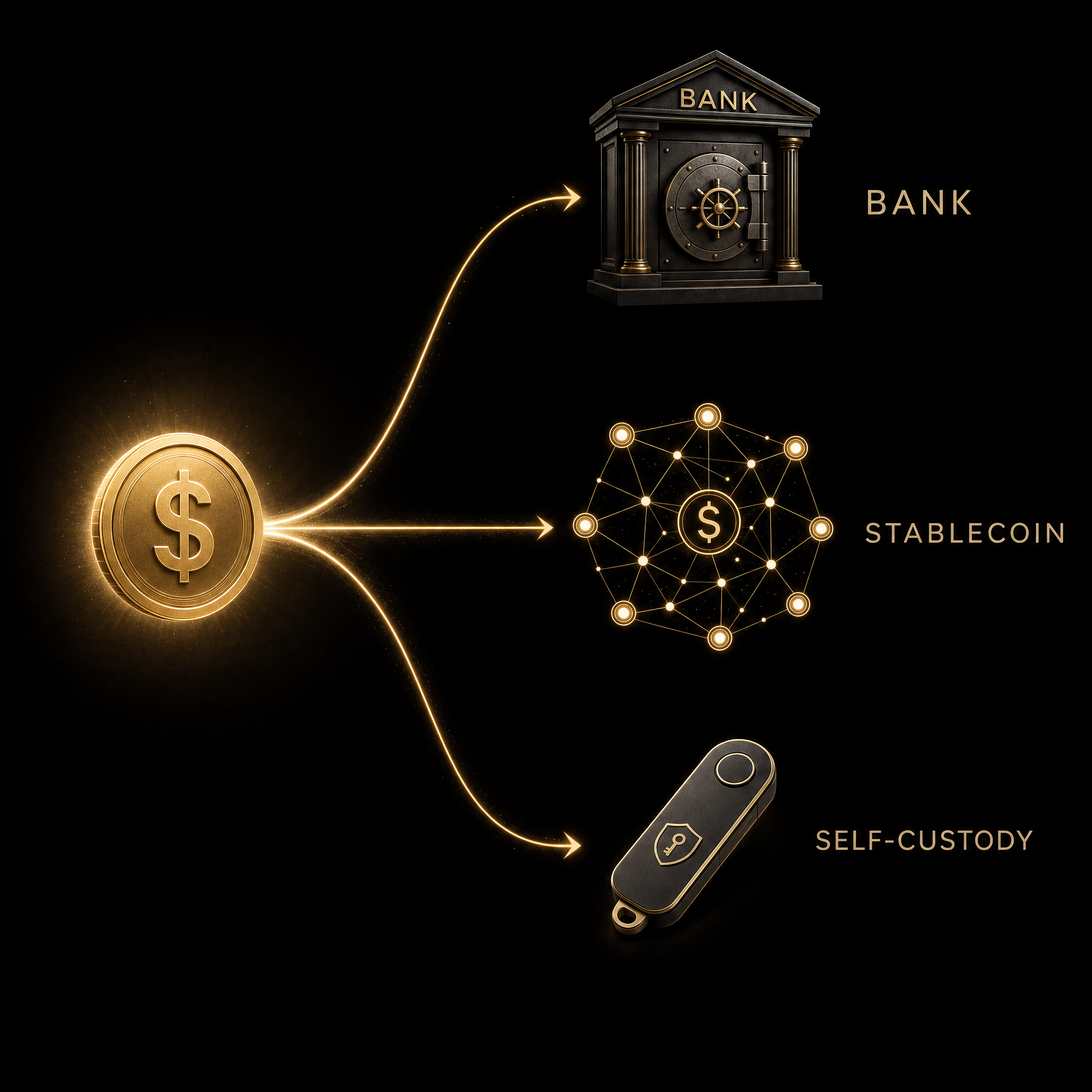

Tokenized Deposit vs. Stablecoin

This is the distinction that matters, and most coverage blurs it. A stablecoin is the liability of a private issuer, a fintech, not your bank, backed by reserves and living on open public chains, generally without FDIC insurance. A tokenized deposit is the liability of your regulated, insured bank (Finovate).

The mechanical difference is where your money physically sits. When you convert cash into a stablecoin, the cash leaves your bank and moves into the issuer’s reserves, liquidity literally drains off the bank’s balance sheet. A tokenized deposit never leaves; it stays on the bank’s books, still usable for lending (BIS). For you, that means a tokenized deposit is the safer-feeling option on insurance and regulation, while a stablecoin gives up that protection in exchange for living on open, permissionless rails.

A tokenized deposit is a better checking account. A stablecoin is a different kind of dollar. Knowing which one you are holding is the whole game.

Break The Ordinary

Why They Are Building It Right Now

Follow the money fear. Jefferies estimates stablecoins could drive a 3% to 5% runoff in core bank deposits over five years and shrink average bank earnings by roughly 3% (CoinDesk). Deposits are the raw material banks lend against; lose them and you lose the business. The stablecoin market has already grown from about $4 billion in 2020 to roughly $320 billion today, and we covered how large that has become in our look at the stablecoin market now exceeding the FX reserves of 95 nations.

The legal door opened too. As TD Securities’ Reid Noch put it, “Following the GENIUS Act, a competition seems to be emerging between stablecoins, tokenized deposits and tokenized money market funds” (CoinDesk). We have watched this same shift in real time, SoFi putting a bank-issued stablecoin in its app, MoneyGram launching a self-custodial dollar, and Paxos clearing stock trades on-chain. The banks are the last big incumbent to move, and they are moving defensively.

What Changes for You, and What Doesn’t

What improves is convenience. Once this network is live, transfers between participating banks could settle instantly, around the clock, instead of waiting for business hours or batch windows. Programmable payments, money that releases automatically when a condition is met, become possible inside the insured banking system. That is genuinely useful.

What does not change is the nature of the thing. A tokenized deposit is still a claim on a bank. It can be frozen, it requires permission, and it is fully visible to the issuer. That is fine for the money you spend and the money you keep liquid, it is what a checking account is for. But it is the opposite of an asset you hold yourself.

Disclosure: the link below is an affiliate link. If you buy through it, Break The Ordinary may earn a commission at no extra cost to you. We only recommend products we would use ourselves.

That contrast is the real lesson here. When the most powerful banks in the country race to build a permissioned digital dollar, the thing they are defending against, a dollar you can hold and move without anyone’s permission, is worth understanding on its own terms. The disciplined approach is not either-or. Use the regulated, insured system for daily money, and for the portion of your wealth you want to truly own, hold it yourself. If part of that is crypto, self-custody in a hardware wallet like the Trezor Safe 5 keeps it off everyone else’s balance sheet, the same control principle we covered in eToro’s move into self-custody.

Three Kinds of Digital Dollar, Side by Side

Tokenized Bank Deposit

- Issuer: Your regulated bank

- Insurance: FDIC-insured

- Control: Permissioned, freezable

- Best for: Daily spending and liquidity

Stablecoin

- Issuer: Private fintech

- Insurance: Generally none

- Control: Open chains, varies by issuer

- Best for: Fast, global, on-chain movement

Self-Custodied Crypto

- Issuer: No one, you hold it

- Insurance: None; you are the bank

- Control: Fully yours, permissionless

- Best for: Long-term ownership you control

Frequently Asked Questions

What is a tokenized deposit?

It is an ordinary bank deposit recorded on a blockchain ledger instead of a traditional one. It stays inside the regulated banking system, remains FDIC-insured, and carries your bank’s protections, but it can settle instantly, 24/7, because it is now a programmable token.

Is a tokenized deposit the same as a stablecoin?

No. A stablecoin is issued by a private company and generally has no FDIC insurance. A tokenized deposit is issued by your regulated, insured bank. The token moves the same way, but the safety net and the issuer are completely different.

Is my money safer in a tokenized deposit?

On insurance and regulation, a tokenized deposit keeps the same FDIC protection and bank oversight you already have. It does not add risk relative to a normal deposit. What it does not give you is independent ownership, it is still a claim on a bank that can be frozen.

Why are the banks building this now?

To defend their deposit base. Jefferies estimates stablecoins could drain 3% to 5% of core bank deposits over five years. After the GENIUS Act opened the regulatory door, tokenized deposits became the banks’ way to match stablecoin speed without losing the money off their balance sheets.

When will it be available?

The shared network through The Clearing House targets the first half of 2027. Exactly which features reach everyday customers, and when, will depend on each participating bank’s rollout.

Should I do anything differently with my money?

Not urgently. Treat a tokenized deposit as a faster checking account when it arrives. The bigger takeaway is structural: use the regulated system for daily money, and for wealth you want to truly own, hold assets you control directly rather than relying only on claims against an institution.

How I Know This

I came to this country as an immigrant and learned the banking system from the outside in, the hard way, every fee, every hold, every “funds available in 3–5 business days.” So I read a story like this with two reactions at once. First, real appreciation: instant, around-the-clock settlement inside an insured system would have saved me a lot of anxious weekends waiting on money to clear.

Second, a habit I never drop: ask who is in control. A faster bank dollar is still a bank dollar. The lesson that built whatever independence I have is to separate the money I move from the money I own, and to keep a meaningful share of the second kind where no institution’s permission is required. This announcement does not change that rule. It sharpens it.

The Bottom Line

The biggest banks in America building a shared blockchain is a real milestone, not because it changes what a dollar is, but because it confirms where money is heading. Tokenized deposits will make the regulated system faster and more flexible, and that is a genuine win for everyday banking. Just keep the distinction straight: this is a better way to move the money you keep at a bank, not a substitute for owning assets outright.

That clarity is what Break The Ordinary exists to give you. Learn the financial fundamentals, use each tool for the job it is actually good at, and make sure that somewhere in your plan there is wealth that is yours, not just a claim on someone else’s balance sheet.

Randal is the founder of Break The Ordinary, where he documents what actually works for building independence. As an immigrant who built from scratch, he reads banking-system news through the lens of someone who learned the difference between moving money and owning it the hard way. He writes from real experience, not hype.